Trade Policy Impacts on U.S. Energy Becoming Visible

September 20, 2018

(from API.org)

In API’s latest Industry Outlook and Monthly Statistical Report, we have shifted from recognizing risks on the horizon to having a line of sight on some of them. The effects of trade disputes in particular have become tangible.

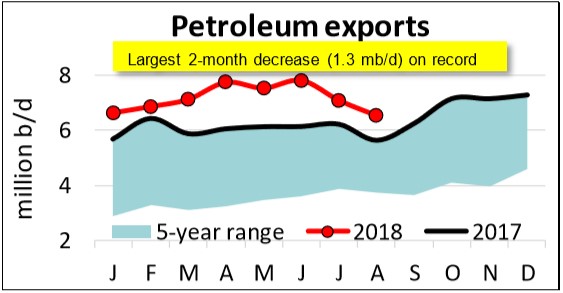

Most notably, at the same time as the U.S. celebrated another new record for crude oil production of 10.8 million barrels per day (mb/d), U.S. petroleum exports decreased by 1.3 mb/d over the past two months.

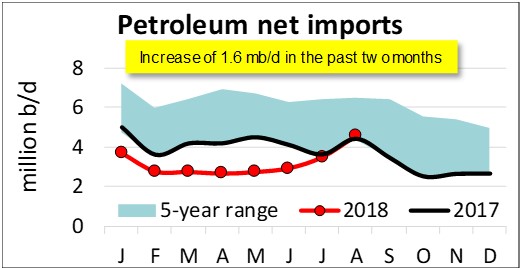

On top of the decline in exports, U.S. imports of refined products also went up by 0.3 mb/d. In total, the United States’ petroleum trade balance went from net imports of 2.9 mb/d in June to 4.5 mb/d in August, which is more than a 56 percent increase in two months that effectively undid a full year’s worth of progress in bringing down U.S. petroleum net imports.

The natural question is why U.S. petroleum trade balance has degraded. The increase in imports could be interpreted as a sign of strong demand and economic growth. However, the decline in exports is potentially of greater concern. While the picture is still a bit muddied, it seems to be getting clearer – the trade war appears to be limiting the United States’ access to crude export markets, or at least temporarily shifting global buying patterns. This is important because, as we produce more energy here at home, the U.S. needs markets for its products. There’s no question that a 1.6 mb/d increase in petroleum net imports is a setback to the United States’ goal of energy dominance.

Some of the administration’s other trade and tariff policies – including steel that’s closely associated with energy development – also raise concern.

Many natural gas and oil producers have reported how their costs have risen. For example, prices of many tubular and specialty steel products, which are main inputs to pipelines, refineries and natural gas liquefaction and petrochemical facilities, increased by more than 25 percent as import tariffs were recently imposed on them. These are materials and components that are largely unavailable domestically and are necessary to complete new projects and ensure the safety and integrity of existing operations.

These cost increases impact far more than the energy industry. The U.S. Bureau of Labor Statistics reported for August that the Producer Price Index for all steel product manufacturing from purchased steel increased by 22.3 percent compared with August 2017. By contrast, this same index was up by only 3.1 percent as of February 2018 versus the same month one year ago, so what we’re seeing in the most current data is a direct and costly effect of the Trump Administration’s tariffs on imported steel.

Another factor that affects markets including energy broadly is the interrelated combination of the recent increases in price inflation, interest rates, the U.S. dollar’s foreign exchange value, and ultimately the costs that consumers and businesses face. These forces, in turn, drive consumption, investment, and economic growth. Although U.S. economic growth has been solid so far in 2018, the Bloomberg consensus expects growth to slow over the next two years as the economy grapples with these headwinds.

A strong U.S. dollar generally has corresponded with lower oil prices in recent years, and prices eased in Q3 2018 despite what appeared to be a tighter global supply/demand balance based on estimates from the U.S. Energy Information Administration (EIA). Supply challenges have emerged from abroad, with OPEC output declines in Venezuela and Angola, plus the impending renewal of sanctions against Iran. In the third quarter and year-to-date through 2018, the U.S. supplied virtually all global oil demand growth.

U.S. consumers also have continued to receive a discount with domestic oil prices of more than $9 per barrel below international ones as of mid-September, which is made possible only because the U.S. has strong domestic oil production.

Shifting to U.S. natural gas markets, as we highlighted last month, U.S. natural gas production increased by more than 9 billion cubic feet per day (Bcf/d) or 12 percent in August compared with August 2017. American technology and process innovations have enabled this growth while lowering prices. Natural gas breakeven costs below $2 per million BTU (mmbtu) were impossible just a few years ago, unless a well also produced significant amounts of oil or natural gas liquids (NGLs) that raised its output value. But according BTU Analytics, the breakeven costs to drill a gas well in the Appalachian basin (Marcellus/Utica formations in Pennsylvania, Ohio and West Virginia) and the Haynesville formation (Texas, Louisiana and Arkansas) were below $2 per mmbtu in July 2018.

By EIA estimates, natural gas prices also fell to an average of $3.03 mmbtu in Q3 2018 from $3.06 per mmbtu in Q3 2017. The low prices stimulated natural gas demand growth for electricity generation and exports of U.S. liquefied natural (LNG), which the EIA estimates increased by 1.8 Bcf/d in Q3 2018 compared with Q3 2017.

The expansion of natural gas and oil production has benefitted the U.S. economy by providing abundant and affordable primary energy sources and an engine of economic activity to major producing states like Texas, Oklahoma, New Mexico, Colorado, North Dakota, Pennsylvania, Ohio, Louisiana, and others.

As with petroleum exports, however, sustaining and growing these benefits largely depends on market growth – to add production that production must have new and/or growing markets to supply, and policy can affect the potential for that market growth.

The future of many U.S. LNG export projects could be challenged if China, which is the largest growing potential buyer, retaliates against the U.S. with an announced 25 percent tariff on U.S. natural gas exports. In turn, this could undermine hundreds of billions of dollars in potential investments for LNG export projects and their supporting infrastructure.

Moreover, the U.S. Energy Department’s (DOE) continued push to bail out failing coal and nuclear plants would squeeze the potential domestic market for natural gas, which could further stymie U.S. production growth and many of the economic benefits it delivers.

With the right policies in place, the U.S. natural gas and oil industry can continue to bring a range of benefits to American consumers, manufacturers and other business sectors while also continuing to lead progress on reducing greenhouse gas emissions. However, this is a critical juncture for the U.S. energy renaissance, as we need cogent energy and trade policies to sustain it, including:

- Smart and forward-looking trade policies that foster access to global markets – as opposed to tariffs and other trade barriers that increase industry costs and disadvantage U.S. natural gas in the global market.

- A level playing field in which fuels can compete in the power generation sector. Policymakers must resist calls for subsidies and/or other market interventions that favor one fuel over another.

Give Us Your Thoughts